Hydrogen for ASEAN Countries’ Clean Energy Transition in Road Transport Sector

Share Article:

Print Article:

By Dr Yanfei Li:

The road transport sector faces challenges in both energy security and environmental concern

According to International Energy Agency (IEA), the Association of Southeast Asian Nations (ASEAN) currently consumes 4.5 million barrels of oil per day, and over 40% of this demand is met by imports. Such oil demand is mainly driven by the transport sector, especially land transport. Importing fossil fuel not only increases insecurity of energy supply, but also burdens ASEAN’s financial and fiscal systems. GHG emissions and urban air quality issues add further to the concerns about the reliance on fossil fuel for transport.

While ASEAN has emphasized biofuels as a form of relief to this problem, the amount that liquid fuels can be blended with biofuels is limited. Currently, the most aggressive plan is to reach 20% of blending.

Electrifying road vehicle fleets with battery electric vehicles (BEV) also comes with intrinsic limitations. Issues with costs, energy density, and short lifetime of batteries are just with the tip of the iceberg. If electricity is not generated by energy sources that are sufficiently clean and green, BEV will cause more emissions and pollution than fossil fuel-powered vehicles. Further long-term problems are stemming from limited global reserves of key battery manufacturing materials and the recycling of a million tonnes of used batteries.

Hydrogen offers another pathway to electrify road transport

The concept of hydrogen fuel cell electric vehicles (FCEV) offers an alternative option towards electrifying the road transport sector with several intrinsic advantages:

First, its energy intensity is higher than that of gasoline. Five kilograms of hydrogen can sustain driving a sedan up to 500 kilometers.

Second, refueling can be done as quickly as gasoline and diesel. These two advantages make it especially suitable for long-distance or heavy-duty trips, such as intercity buses and cargo delivery by trucks.

Third, hydrogen can be produced by various means, especially from clean and locally available sources such as solar, wind, hydropower, nuclear energy, and biomass.

Fourth, hydrogen as an energy storage is flexible in terms of both scale, location, and timing. It is thus complementing intermittent as well as seasonal renewable energy such as hydro, solar, wind, and biomass. Integrating hydrogen as part of the energy system could thus strategically enhance its flexibility and security.

In this regard, according to estimations from various reports, ASEAN possesses 229 GW of theoretical resources of wind energy, 158 GW of hydropower (including small hydro), 61 GW of biomass, and 200 GW of geothermal. In regard to solar energy, ASEAN plans to install 55 GW by 2025, while Indonesia alone is predicted to develop 47 GW of capacity by 2030, according to International Renewable Energy Agency (IRENA). An Asian Development Bank (ADB) report indicated 8 GW of technical potential of solar power in Cambodia, while IRENA indicated over 10 GW of potential for Lao PDR and over 25 GW in the case of Viet Nam.

Intermittent renewables can be used to produce hydrogen, not only to serve as a zero-emission fuel to power vehicles, but also to function as a long-term and large-scale energy storage and thus stabilize the power grid system which expects in-depth penetration of these renewables in the future.

Gaps in Maturity and Costs of Technologies are Closing Fast

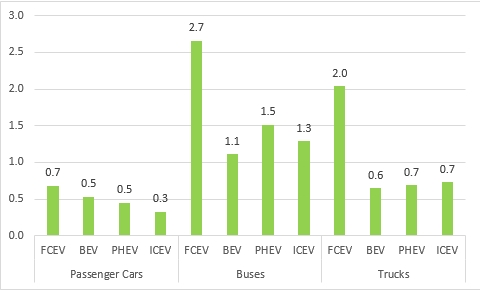

Admittedly the hydrogen supply chain and related technologies are still expensive at this moment. According to a recent study by the Economic Research Institute for ASEAN and East Asia (ERIA), specifically in ASEAN, the total cost of owning and driving a hydrogen-powered fuel cell vehicle is two to three times as high as a conventional gasoline or diesel vehicle, depending on the vehicle fleet (passenger vehicle, bus, or truck), scenario of vehicle usage, and pathway of hydrogen supply, as Figure 1 shows.

Figure 1: Average Vehicle Total Cost of Ownership ($/km) in ASEAN Today

Note: Total cost of ownership averages the costs of purchasing and operating the vehicle against its total mileage over its lifetime. $ indicates U.S. dollar. FCEV stands for fuel cell electric vehicle. BEV stands for battery electric vehicle. PHEV stands for plug-in hybrid electric vehicle. ICEV stands for internal combustion engine vehicle.

Source: ERIA

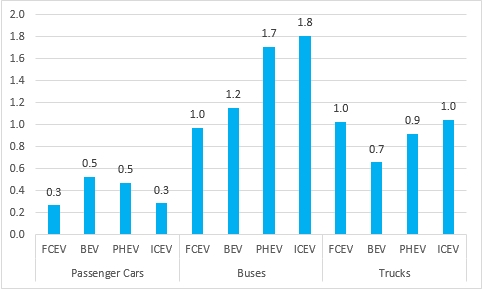

However, in line with mainstream projections about future development of hydrogen-related technologies as well as the learning effect and economy-of-scale to be achieved by the industry, ERIA’s study revealed that by around 2030, the gap in costs between conventional vehicles and hydrogen-powered vehicles will largely be bridged, as Figure 2 indicates.

Figure 2: Average Vehicle Total Cost of Ownership ($/km) in ASEAN by 2030

Source: ERIA

Policies to encourage low emission vehicles, pricing GHG emissions, or putting surcharges on conventional vehicles and fossil fuels will further add to the competitiveness of hydrogen and FCEV. The turning point for hydrogen-based mobility to become competitive is approaching on a fast track.

An Opportunity to Leapfrog in Investing the Next-generation Clean Energy Infrastructure

Prospects of disruptive technologies are typically self-realizing: the more people believe in it, the sooner it comes. Several main energy consuming countries such as China, Germany, Japan, and South Korea now seem to share a common vision about hydrogen. These countries have just recently renewed their initiatives on hydrogen, moving quicker to demonstrate early-stage commercial applications and accordingly deploy supply chain of hydrogen and its related technologies. In its recently announced 2050 long-term climate change strategy, the European Union has perceived hydrogen as a critical element to build its future net zero-emission energy system.

This global development about hydrogen initiatives coincides with ASEAN’s announced ambition to achieve 23% renewable energy integration into its energy system by 2025, and even more by 2030. Such a major energy transition poses a major question as what kind of energy infrastructure to be laid down. If clean and green energy is a determined future for ASEAN countries, it is time now to seriously consider integrating hydrogen technologies in future transport as well as power system and coupling them with the development of renewable energy. This will give ASEAN countries opportunities to not only leapfrog in developing a future-oriented energy infrastructure, but also foster ASEAN as a future hub for catering global supply chains for clean and green energy technologies.

-------

This opinion piece was written by Dr Yanfei Li, and has been published in China Daily. Click here to subscribe to the monthly newsletter.